Integrated Reporting

INTRODUCTION AND PURPOSE

The corporate world has seen lot of metamorphosis. The simplistic pattern of reporting, as was established in the post-world war II arena no longer serves the purpose. Change, as they say, is the only constant in the world and so for Reporting- to stakeholders, across categories.

Through the myriad structural changes in the economy, in corporate functioning, and complicated web of information, although the complex business environment is interconnected, it has become imperative to acknowledge that sustainable development is a critical part of good governance.

The existing corporate reporting structure focusses on disseminating sufficient levels of information to the stakeholders. However, there needs more coverage under the reporting framework, that will ensure value creation and communication of factors impacting value creation. This will enable higher levels of transparency and facilitate robust decision making by the stakeholders.

This strategic reporting need, has facilitated the reporting framework — Integrated Reporting.

We need to understand, the level at which Corporate Reporting stands today and how Integrated Reporting will forge Value Creation and Sustainable Development.

CORPORATE REPORTING TODAY

Corporate Reporting aims at providing credible information to stakeholders thereby bringing about greater accountability and transparency. This information, if complete, helps in making decisions that facilitate future business ventures.

The current reporting framework helps an organization

1. Better access to capital and finance

2. Reduced costs

3. Facilitating better stakeholder relationships

4. Development of trust among the internal stakeholders — e.g.: Employees.

The information function of the reporting focusses on information dissemination and the transformation function envisages feedback on the information that helps tweak the corporate behavior to achieve benefits.

The Corporate Reporting function in its current form has undergone various stages of evolution and has been adjusted to changing environment at various periods of time. The Financial Statements continue to be the cornerstone of the reporting function and along with management commentary, governance synopsis and financial footnotes have resulted higher levels of value creation for stakeholders.

Yet, there is an enhanced need for understanding the non-financial material risks that are involved therein.

The tangible assets form only 20% of the overall resources of a company — the contribution of the intangible assets to the form a major component of the value creation for a company is missed out in the current reporting structure

This inadequacy in the current reporting framework elicits the need for a new 21st Century form of reporting — Integrated Reporting.

INTEGRATED REPORTING FRAMEWORK

An Integrated report is a single document that details out the complete set of financial and Non-Financial information regarding a company in order to provide a holistic view of the company.

Quoting from the IMA Statement on Integrated Reporting. An integrated report is developed in response to stakeholder groups and investors’ need for enhanced reporting that connects strategy, risks, key performance indicators (KPIs), and financial performance. Providing an integrated report is an effective “way of communicating to all stakeholders that the company is taking a holistic view of their interest.

It helps a company demonstrate strategy, governance, risks, transformation, prospects, KPIs and value with the external environment impacts, in the short, medium and long terms. In essence as the International Integrated Reporting Council (IIRC) mentions, the report shows all the aspects and how limited capital resources are impacted and a view of the business model

SALIENT FEATURES AND PRINCIPLES

The IIRC has prescribed the following seven guiding Principles which underpin the preparation of an integrated report.

Strategic Focus and Future Orientation

An integrated report should provide insight into the organization’s strategy and how it relates to the organization’s ability to create value in the short, medium and long term and to its use of and effects on capital.

Connectivity of information

It often gives a complete idea about the combination, interrelatedness and dependencies between the factors that affect the organization’s ability to create value over time. Some types of interconnected information are represented as below

· Holistic view of the organization proceedings

· A detailed view of the past, present and planned activities of an organization

· The combination or interrelatedness of all forms of Capitals and their impact on the value creation outcomes.

Stakeholder relationships

An integrated report should provide insight into the nature and quality of the organization’s relationships with its key stakeholders, including how and to what extent the organization understands, takes into account and responds to their legitimate needs and interests.

Materiality

An integrated report should disclose information about factors that have a substantial impact on the organization’s ability to create value over the short, medium and long term.

Materiality is one of the most important guiding principles. It warrants that all factors that are “Material” or substantial must be included in the report. Examples may be reporting of Strength, weakness, opportunities, threats, risks — present and future, trend line on the organisation’s future activities.

What “Material” is, must be decided with the consensus of all the actors involved in the Integrating reporting process.

Conciseness

An Integrated report is concise and relevant. One must avoid using jargons and technically complicated terminology.

· Prioritize factors that concern materiality

· Ensure reporting is consistent in its flow of information

· Clarity of concepts

Reliability and completeness

An integrated report should include all material matters, both positive and negative, without any error in the reporting of the material facts concerning the report. Control mechanisms, like inspections, audits, internal controls can ensure reliability of the information that is being reported

Consistency and comparability

The information in an integrated report should be presented: (a) on a basis that is consistent overtime; and (b) in a way that enables comparison with other organizations to the extent

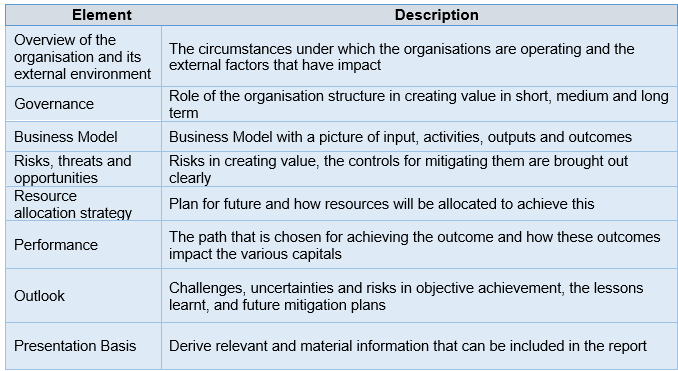

Integrated reporting is all about Creation of Value. The Salient Features of Creation of Value can be enumerated as given below. These will form the core elements of Integrated Reporting.

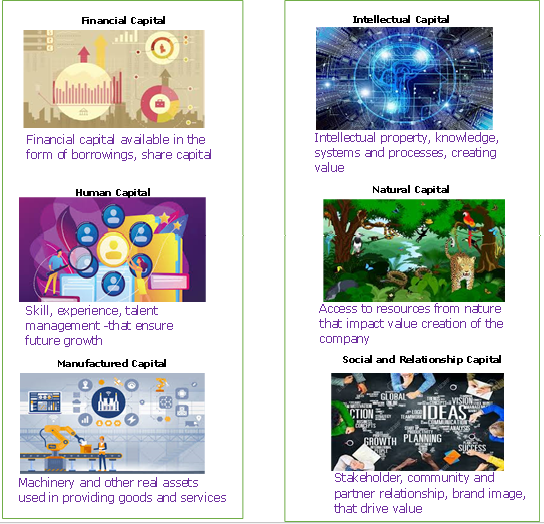

TYPES OF CAPITAL

In the integrated reporting — Integrated thinking framework, the value creation is not dependent on Financial Capital alone. It is dependent on other forms of capital as well. These capitals drive value over time and grow in capacity if leveraged properly

Researchers have found that providing credible information is associated with better access to financing, lower cost of capital, better business relations with customers and suppliers, and greater trust from employees. Therefore, a major function of corporate reporting is to provide all stakeholders with the information they require to conduct business transactions — defined as the “information function” of corporate reporting. Yet corporate reporting has a second function that goes a step further in the process of information disclosure i.e. Sustainable Development

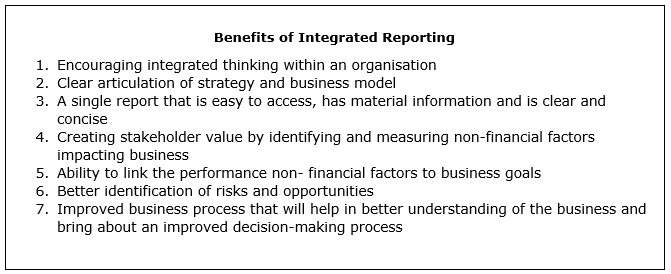

BENEFITS OF INTEGRATED REPORTING AND THINKING

INTEGRATED REPORTING AND SUSTAINABLE DEVELOPMENT GOALS (SDG)

The United Nations Conference on Trade and Development (UNCTAD) and the International Integrated Reporting Council (IIRC) are working together to help companies report their performance in the light of the world moving towards achieving the Sustainable Development Goals(SDGs).

The UNCTAD is responsible for accounting the reporting within the UN and the IIRC is promoting the Integrated Reporting and Integrated Thinking Framework — a holistic form of reporting value generated by business, which is much beyond Financial Value. These will help the world achieve the SDGs and enable organizations contribute in multiple forms and using various capitals in forging sustainable growth.

The 17 Sustainable Development Goals identified in the UN Summit of 2015 are:

Goal 1: No Poverty

Goal 2: Zero Hunger

Goal 3: Good Health and Well- Being

Goal 4: Quality Education

Goal 5: Gender Equality

Goal 6: Clean Water and Sanitation

Goal 7: Affordable and Clean Energy

Goal 8: Decent Work and Economic Growth

Goal 9: Industry, Innovation and Infrastructure

Goal 10: Reduced Inequalities

Goal 11: Sustainable Cities and Communities

Goal 12: Responsible Consumption and Production

Goal 13: Climate Action

Goal 14: Life Below Water

Goal 15: Life on Land

Goal 16: Peace, Justice and Strong Institutions

Goal 17: Partnerships

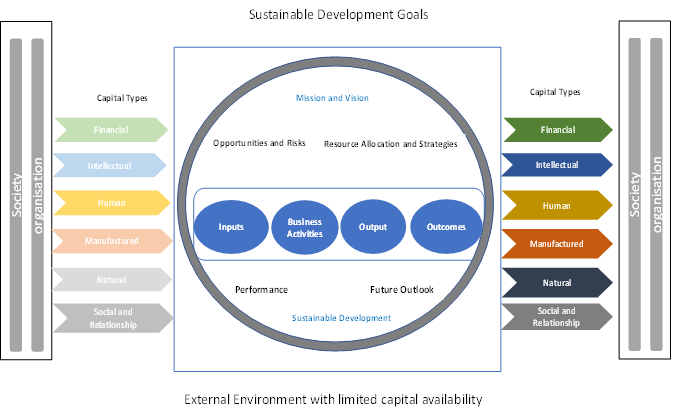

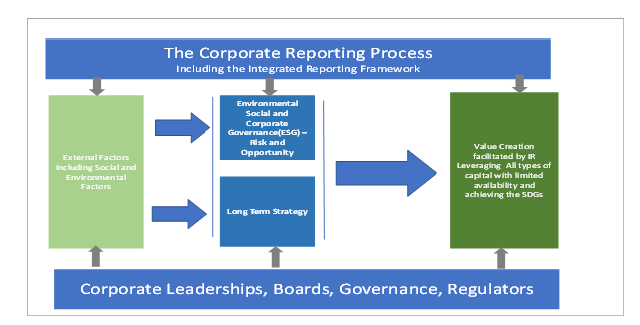

These 17 goals have been further subdivided into 169 Targets that underpin the delivery of the SDGs. As an example the one of the Targets (Target 12.6) under the Goal 12 is: “Encourage companies to adopt sustainable business practices and sustainability reporting”. The interdependence between Integrated Reporting, SDGs, External Factors and Environmental, Social and Corporate Governance (ESGs) is described in the figure below

Considering the above interdependence, organizations need to follow these Steps to achieve the SDGs

1. Understanding: Organization’s external environment and issues they pose for sustainable development

2. Identify sustainable development issues that are material and influence value creation

3. Develop Business Models strategy that can facilitate achieving the SDGs

4. Develop a model of Integrated Thinking, Connectivity and Governance

WHAT THE FUTURE HAS IN STORE

There will be movement towards IR considering the benefits and there can be enablement, facilitation and pressure on companies to implement. How each stakeholder can facilitate the same is elicited below

ACTIONABLE FROM INTERNAL AUDIT

An integrated report helps build a sustainable and resilient organization by shifting the focus from meeting short-term financial goals to meeting long-term strategic and sustainability goals.

While the management, board, and technology are key to effective integrated reporting, the Internal Audit function can play a prominent and proactive role by providing assurance and advice related to governance and the processes required to create an integrated report.

In order to achieve this, Internal Audit may have to expand its current capabilities. However, it is uniquely positioned in the organization to enable effective integrated reporting and improving business performance.

INTEGRATED REPORTING IN INDIA

The Indian perspective

On 7 February 2017, SEBI (Securities and Exchange Board of India) has issued a circular advising top 500 listed companies which are required to prepare BRR (Business Responsibility Report) to adopt IR on a voluntary basis from the financial year 2017–18.

The information related to IR may be provided in the following ways:

As part of annual report with a separate section on IR

Incorporating in management discussion and analysis, or

By preparing a separate report (annual report prepared as per IR framework)

In case the company has already provided the relevant information in any other report prepared in accordance with national/international requirement/framework, it may provide appropriate reference to the same in its integrated report so as to avoid duplication of information.

A study on integrated reporting amongst banks and found that the extent of integration amongst most of the Indian banks is limited and they now should move from limited or partial integration to full integration.

The Adoption of IR in India have been good and some examples of the industries that have adopted are as below

This level of adoption is due to the reasons as given below.

1. Ownership taken by Boards — Benefits of value creation are visible. There is collaboration between GRC and Strategy and policy formation

2. Measurement of the leverage and Impact of the use of the various capitals

3. Value creation of Business Models and Strategies are being reported especially on Natural and Social Capitals

4. Improved quality of presentation due to technology use.

The same reasons also ensure that the future of Integrated Reporting augurs well in India and this will ensure we can fast-track the achievement of the SDG targets and Goals and the ESG risks become opportunities.

CONCLUSION

For emerging fast growing nations like India the challenge will be to aggressively grow the economy, invest in infrastructure, skill and education to meet the aspirations of a burgeoning middle class and millennial population.

At the same time understand and influence the trade-offs — depleting forest cover, water scarcity, poor air quality, climate vulnerabilities and income inequality. Therefore, this momentum towards better reporting should continue to progress with more companies embracing the framework and the integrated thinking approach that would enable an outcome based holistic view of how they create value for themselves and the extended society.

References

https://www2.deloitte.com/uk/en/pages/audit/articles/integrated-reporting.html :

Insightful Blog Posts

INTRODUCTION AND PURPOSE

The corporate world has seen lot of metamorphosis. The simplistic pattern of reporting, as was established in the post-world war II arena no longer serves the purpose. Change, as they say, is the only constant in the world and so for Reporting- to stakeholders, across categories.

Through the myriad structural changes in the economy, in corporate functioning, and complicated web of information, although the complex business environment is interconnected, it has become imperative to acknowledge that sustainable development is a critical part of good governance.

The existing corporate reporting structure focusses on disseminating sufficient levels of information to the stakeholders. However, there needs more coverage under the reporting framework, that will ensure value creation and communication of factors impacting value creation. This will enable higher levels of transparency and facilitate robust decision making by the stakeholders.

This strategic reporting need, has facilitated the reporting framework — Integrated Reporting.

We need to understand, the level at which Corporate Reporting stands today and how Integrated Reporting will forge Value Creation and Sustainable Development.

CORPORATE REPORTING TODAY

Corporate Reporting aims at providing credible information to stakeholders thereby bringing about greater accountability and transparency. This information, if complete, helps in making decisions that facilitate future business ventures.

The current reporting framework helps an organization

1. Better access to capital and finance

2. Reduced costs

3. Facilitating better stakeholder relationships

4. Development of trust among the internal stakeholders — e.g.: Employees.

The information function of the reporting focusses on information dissemination and the transformation function envisages feedback on the information that helps tweak the corporate behavior to achieve benefits.

The Corporate Reporting function in its current form has undergone various stages of evolution and has been adjusted to changing environment at various periods of time. The Financial Statements continue to be the cornerstone of the reporting function and along with management commentary, governance synopsis and financial footnotes have resulted higher levels of value creation for stakeholders.

Yet, there is an enhanced need for understanding the non-financial material risks that are involved therein.

The tangible assets form only 20% of the overall resources of a company — the contribution of the intangible assets to the form a major component of the value creation for a company is missed out in the current reporting structure

This inadequacy in the current reporting framework elicits the need for a new 21st Century form of reporting — Integrated Reporting.

INTEGRATED REPORTING FRAMEWORK

An Integrated report is a single document that details out the complete set of financial and Non-Financial information regarding a company in order to provide a holistic view of the company.

Quoting from the IMA Statement on Integrated Reporting. An integrated report is developed in response to stakeholder groups and investors’ need for enhanced reporting that connects strategy, risks, key performance indicators (KPIs), and financial performance. Providing an integrated report is an effective “way of communicating to all stakeholders that the company is taking a holistic view of their interest.

It helps a company demonstrate strategy, governance, risks, transformation, prospects, KPIs and value with the external environment impacts, in the short, medium and long terms. In essence as the International Integrated Reporting Council (IIRC) mentions, the report shows all the aspects and how limited capital resources are impacted and a view of the business model

SALIENT FEATURES AND PRINCIPLES

The IIRC has prescribed the following seven guiding Principles which underpin the preparation of an integrated report.

Strategic Focus and Future Orientation

An integrated report should provide insight into the organization’s strategy and how it relates to the organization’s ability to create value in the short, medium and long term and to its use of and effects on capital.

Connectivity of information

It often gives a complete idea about the combination, interrelatedness and dependencies between the factors that affect the organization’s ability to create value over time. Some types of interconnected information are represented as below

· Holistic view of the organization proceedings

· A detailed view of the past, present and planned activities of an organization

· The combination or interrelatedness of all forms of Capitals and their impact on the value creation outcomes.

Stakeholder relationships

An integrated report should provide insight into the nature and quality of the organization’s relationships with its key stakeholders, including how and to what extent the organization understands, takes into account and responds to their legitimate needs and interests.

Materiality

An integrated report should disclose information about factors that have a substantial impact on the organization’s ability to create value over the short, medium and long term.

Materiality is one of the most important guiding principles. It warrants that all factors that are “Material” or substantial must be included in the report. Examples may be reporting of Strength, weakness, opportunities, threats, risks — present and future, trend line on the organisation’s future activities.

What “Material” is, must be decided with the consensus of all the actors involved in the Integrating reporting process.

Conciseness

An Integrated report is concise and relevant. One must avoid using jargons and technically complicated terminology.

· Prioritize factors that concern materiality

· Ensure reporting is consistent in its flow of information

· Clarity of concepts

Reliability and completeness

An integrated report should include all material matters, both positive and negative, without any error in the reporting of the material facts concerning the report. Control mechanisms, like inspections, audits, internal controls can ensure reliability of the information that is being reported

Consistency and comparability

The information in an integrated report should be presented: (a) on a basis that is consistent overtime; and (b) in a way that enables comparison with other organizations to the extent

Integrated reporting is all about Creation of Value. The Salient Features of Creation of Value can be enumerated as given below. These will form the core elements of Integrated Reporting.

TYPES OF CAPITAL

In the integrated reporting — Integrated thinking framework, the value creation is not dependent on Financial Capital alone. It is dependent on other forms of capital as well. These capitals drive value over time and grow in capacity if leveraged properly

Researchers have found that providing credible information is associated with better access to financing, lower cost of capital, better business relations with customers and suppliers, and greater trust from employees. Therefore, a major function of corporate reporting is to provide all stakeholders with the information they require to conduct business transactions — defined as the “information function” of corporate reporting. Yet corporate reporting has a second function that goes a step further in the process of information disclosure i.e. Sustainable Development

BENEFITS OF INTEGRATED REPORTING AND THINKING

INTEGRATED REPORTING AND SUSTAINABLE DEVELOPMENT GOALS (SDG)

The United Nations Conference on Trade and Development (UNCTAD) and the International Integrated Reporting Council (IIRC) are working together to help companies report their performance in the light of the world moving towards achieving the Sustainable Development Goals(SDGs).

The UNCTAD is responsible for accounting the reporting within the UN and the IIRC is promoting the Integrated Reporting and Integrated Thinking Framework — a holistic form of reporting value generated by business, which is much beyond Financial Value. These will help the world achieve the SDGs and enable organizations contribute in multiple forms and using various capitals in forging sustainable growth.

The 17 Sustainable Development Goals identified in the UN Summit of 2015 are:

Goal 1: No Poverty

Goal 2: Zero Hunger

Goal 3: Good Health and Well- Being

Goal 4: Quality Education

Goal 5: Gender Equality

Goal 6: Clean Water and Sanitation

Goal 7: Affordable and Clean Energy

Goal 8: Decent Work and Economic Growth

Goal 9: Industry, Innovation and Infrastructure

Goal 10: Reduced Inequalities

Goal 11: Sustainable Cities and Communities

Goal 12: Responsible Consumption and Production

Goal 13: Climate Action

Goal 14: Life Below Water

Goal 15: Life on Land

Goal 16: Peace, Justice and Strong Institutions

Goal 17: Partnerships

These 17 goals have been further subdivided into 169 Targets that underpin the delivery of the SDGs. As an example the one of the Targets (Target 12.6) under the Goal 12 is: “Encourage companies to adopt sustainable business practices and sustainability reporting”. The interdependence between Integrated Reporting, SDGs, External Factors and Environmental, Social and Corporate Governance (ESGs) is described in the figure below

Considering the above interdependence, organizations need to follow these Steps to achieve the SDGs

1. Understanding: Organization’s external environment and issues they pose for sustainable development

2. Identify sustainable development issues that are material and influence value creation

3. Develop Business Models strategy that can facilitate achieving the SDGs

4. Develop a model of Integrated Thinking, Connectivity and Governance

WHAT THE FUTURE HAS IN STORE

There will be movement towards IR considering the benefits and there can be enablement, facilitation and pressure on companies to implement. How each stakeholder can facilitate the same is elicited below

ACTIONABLE FROM INTERNAL AUDIT

An integrated report helps build a sustainable and resilient organization by shifting the focus from meeting short-term financial goals to meeting long-term strategic and sustainability goals.

While the management, board, and technology are key to effective integrated reporting, the Internal Audit function can play a prominent and proactive role by providing assurance and advice related to governance and the processes required to create an integrated report.

In order to achieve this, Internal Audit may have to expand its current capabilities. However, it is uniquely positioned in the organization to enable effective integrated reporting and improving business performance.

INTEGRATED REPORTING IN INDIA

The Indian perspective

On 7 February 2017, SEBI (Securities and Exchange Board of India) has issued a circular advising top 500 listed companies which are required to prepare BRR (Business Responsibility Report) to adopt IR on a voluntary basis from the financial year 2017–18.

The information related to IR may be provided in the following ways:

As part of annual report with a separate section on IR

Incorporating in management discussion and analysis, or

By preparing a separate report (annual report prepared as per IR framework)

In case the company has already provided the relevant information in any other report prepared in accordance with national/international requirement/framework, it may provide appropriate reference to the same in its integrated report so as to avoid duplication of information.

A study on integrated reporting amongst banks and found that the extent of integration amongst most of the Indian banks is limited and they now should move from limited or partial integration to full integration.

The Adoption of IR in India have been good and some examples of the industries that have adopted are as below

This level of adoption is due to the reasons as given below.

1. Ownership taken by Boards — Benefits of value creation are visible. There is collaboration between GRC and Strategy and policy formation

2. Measurement of the leverage and Impact of the use of the various capitals

3. Value creation of Business Models and Strategies are being reported especially on Natural and Social Capitals

4. Improved quality of presentation due to technology use.

The same reasons also ensure that the future of Integrated Reporting augurs well in India and this will ensure we can fast-track the achievement of the SDG targets and Goals and the ESG risks become opportunities.

CONCLUSION

For emerging fast growing nations like India the challenge will be to aggressively grow the economy, invest in infrastructure, skill and education to meet the aspirations of a burgeoning middle class and millennial population.

At the same time understand and influence the trade-offs — depleting forest cover, water scarcity, poor air quality, climate vulnerabilities and income inequality. Therefore, this momentum towards better reporting should continue to progress with more companies embracing the framework and the integrated thinking approach that would enable an outcome based holistic view of how they create value for themselves and the extended society.

References

https://www2.deloitte.com/uk/en/pages/audit/articles/integrated-reporting.html :

Mastering the First Impression: Your intriguing post title goes here

Engaging Introductions: Capturing Your Audience\’s Interest The initial impression your blog post makes is crucial, and that\’s where your introduction…

The Art of Drawing Readers In: Your attractive post title goes here

Engaging Introductions: Capturing Your Audience\’s Interest The initial impression your blog post makes is crucial, and that\’s where your introduction…

Crafting Captivating Headlines: Your awesome post title goes here

Engaging Introductions: Capturing Your Audience\’s Interest The initial impression your blog post makes is crucial, and that\’s where your introduction…

Hello world!

Welcome to WordPress. This is your first post. Edit or delete it, then start writing!